How To Write A Check In The Digital Age

I learned how to write a check when I was in my mid-teens, back when it was exciting having a checkbook. My dad sat me down at the dining room table and walked me through the process—what to write, where to sign. I learned how to write out the dollar amount in words on the correct line and use a fraction for cents (X/100). Three misprinted checks later, I finally sat with a perfect example of my newfound freedom, sloppy cursive aside. It was all so thrilling. A new wave of independence, all linked to my own checking account (which was linked to my parent’s checking account).

Today, checkbooks are almost a thing of the past; it wouldn't be surprising if the majority of millennials had no clue as to how to write a check. With debit cards and online banking and direct deposit (which is how many employees get paid — rather than getting a paper check and bringing it to the bank to deposit it, money is sent directly to the employee’s bank account), it’s hard to see the use of keeping a checkbook. However, there are some big benefits to writing checks instead of resorting to sliding the plastic or handing out gobs of cash.

Writing a paper check versus other forms of payments is great for large purchases, like expensive goods or rent. It can help you not only keep track of your purchases because of the literal papertrail in your checkbook, but it also is safer than using digital means of currency or cash. No one can hack into your checkbook, and only the assigned payee can cash your check. By taking the longhand route, you also have the option to cancel payment or postdate a check so the payee cannot cash it until a particular date. So if someone you paid for a job decided not to make good on the agreed upon services, you can potentially refund yourself by canceling the check before it is cashed. It gives you a little more control over the how, when, and where your money is used, which is always a good thing. Paper checks don’t carry transaction fees like plastic cards do.

There is also a professionalism that accompanies a handwritten check that makes it more appropriate for certain people (like, say, your landlord), than cash or debit.

So now you know the why, what about the how? Let’s get started—start practicing your cursive now.

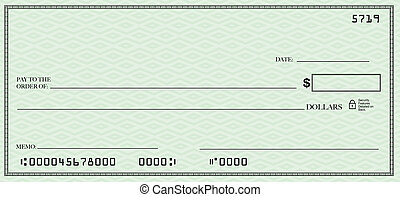

Here is a basic check. At the bottom is the account number and routing number that link to your checking account, and then a check number that corresponds to the (you guessed it) check number in your checkbook. Above those are six areas for you to fill out: date, payee, amount—written out and written numerically--memo, and signature.

First, start by writing the date in the top right corner. Here is where you place the day’s date, or, a future date if you and your payee have agreed that the check is not to be cashed until a later time. This is called post dating and can be important if, say, you don't have enough money in your bank account now, but expect to by the time the check is cashed. It can be necessary for other types of transactions as well, such as expense reports and accounting purposes.

Next, write the person you are paying in the “Pay to the order of” section. This is the payee who is going to cash your check. It can be an individual person or a company. Handwrite the name in a legible print on the designated line.

In the box next to the payee line, you write the amount of money, indicating the dollars and cents numerically. So, if the payment was $19.99, you would write the dollar amount as 19.99.

In the line underneath the payee line is where you write out the value longhand, but only for the dollar amount. The cents are written out numerically again. For example, with that same $19.99 payment, you would write Nineteen and 99/100. Or if the payment was $101.01, you would print One hundred and one 01/100. Add a dash from the end of 100 until the “dollars” to ensure no one adds anything to the end of the check without your permission.

The final mandatory step for writing your check is your signature on the line at the bottom right. After you’ve penned your name, your check is good to go.

But what about the memo line? This is optional, but recommended to keep yourself and your payee aware of what the check is for. Think of it like the comments section in VenMo (without the emojis). You just want to write a word or phrase that reminds you what the payment was for, such as: rent, groceries, landscaper, etc.

Tear off the part of the check you filled out and keep the carbon copy in your checkbook for balancing and referral purposes.

--

Alexandra Deabler is a writer and editor. She has published articles about California history, travel, lifestyle, personal essays, and short fiction. She lives in New York City and can be reached through her website: alexandradeabler.com.

Fairygodboss is committed to improving the workplace and lives of women.

Join us by reviewing your employer!

Why women love us:

- Daily articles on career topics

- Jobs at companies dedicated to hiring more women

- Advice and support from an authentic community

- Events that help you level up in your career

- Free membership, always